Investment

Strategies

BOA Alphaline deploys systematic quantitative investment strategies across global financial markets. Each strategy is independently developed, rigorously tested, and managed within a consistent institutional governance and risk management framework.

Our Investment Methodology

Our investment methodology is rooted in the application of advanced mathematical models and sophisticated statistical analysis to make prudent investment decisions.

It involves using data-driven techniques and algorithmic trading to identify patterns, trends and correlations in data, which are subsequently automated to execute trades seamlessly. The underlying objective is to minimise the impact of behavioural biases and optimise overall portfolio performance.

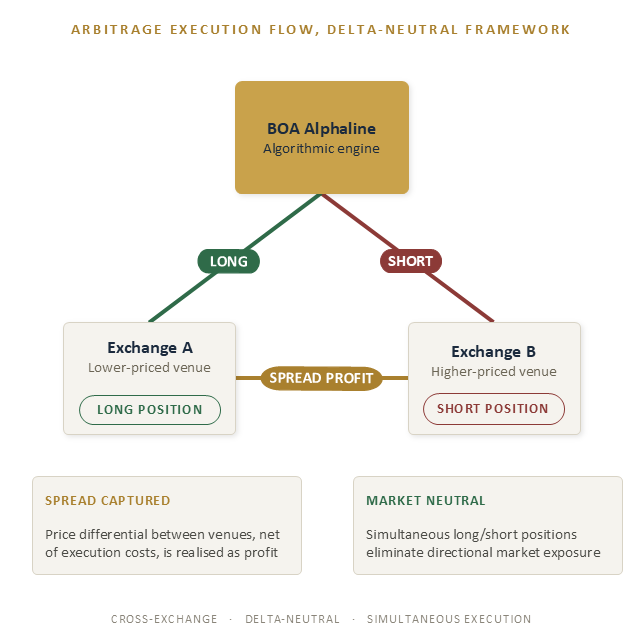

Cross-Exchange Arbitrage

Identifies and captures pricing discrepancies across multiple execution venues. Using a delta-neutral framework, the strategy simultaneously establishes offsetting positions where an asset is priced differently across venues, seeking to profit from spread convergence rather than directional market movements.

The strategy primarily focuses on highly liquid instruments with sufficient market depth and pricing efficiency. Trading instruments are selected based on liquidity, execution quality, and the availability of arbitrage opportunities across multiple venues.

While designed to minimise directional market exposure, the strategy remains subject to execution risk, exchange counterparty risk, technology and connectivity risk, and liquidity risk. Past performance is not indicative of future results.

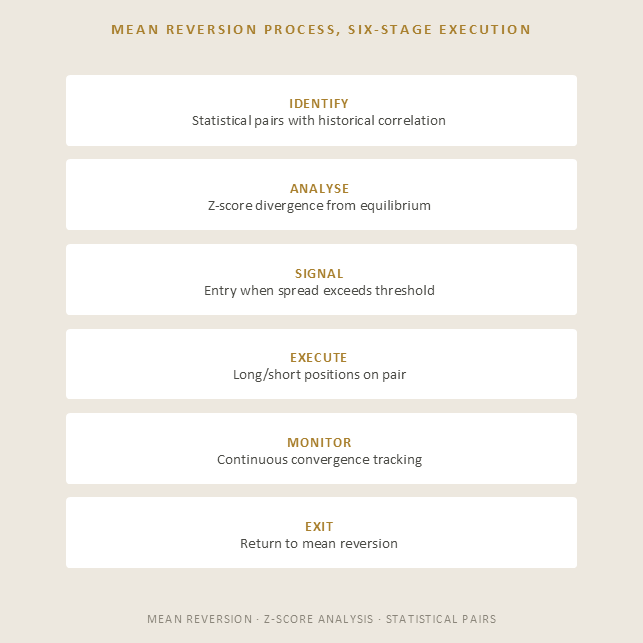

Statistical Arbitrage

The Statistical Arbitrage strategy seeks to identify and capture opportunities arising from temporary deviations in historically observed market relationships. The strategy applies quantitative, rule-based analysis to identify statistical pairs or baskets of instruments with observed historical price relationships.

When deviations from these historical relationships are identified beyond defined statistical thresholds, the strategy seeks to establish positions designed to profit when the relationship mean-reverts. The strategy is systematic and data-driven, with position management governed by predefined risk parameters.

Past performance is not indicative of future results. The strategy is subject to model risk, market risk, and execution risk.

Multi-Strategy Model (MSM)

The Multi-Strategy Model (MSM) is a systematic quantitative investment framework designed to identify opportunities across multiple markets through data-driven research and automated execution.

The model continuously evaluates a broad range of inputs, including order book data, market liquidity, price action, volatility measures, market sentiment, on-chain activity, macroeconomic indicators, and alternative datasets. These factors are analysed through proprietary quantitative models to generate investment signals and allocate capital across multiple independent strategies.

By combining diverse return drivers within a unified portfolio framework, the MSM seeks to enhance diversification, reduce dependence on any single market condition, and maintain a disciplined approach to risk management and capital preservation.

The MSM involves multiple concurrent strategies, each with distinct risk characteristics. The model is subject to market risk, model risk, liquidity risk, and execution risk. Capital allocation across strategies may vary based on prevailing market conditions and risk parameters. Past performance is not indicative of future results.

.PNG)

Request Strategy Documentation

Contact our institutional team to request detailed strategy documentation, operational memoranda, or fund prospectuses.